From EVs and batteries to autonomous vehicles and urban transport, we cover what actually matters. Delivered to your inbox weekly.

The UK automotive market has reached a new milestone in electrification: two out of every five new car models now available are fully battery electric.

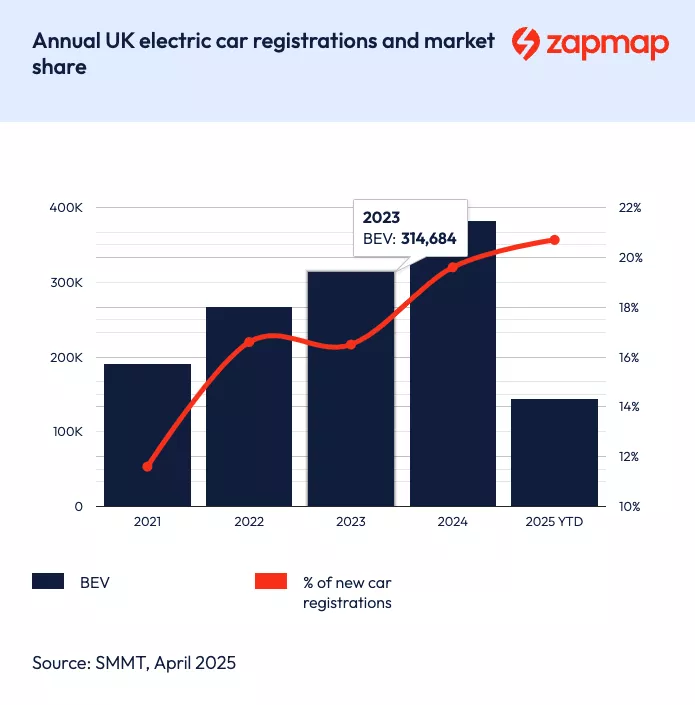

According to the Society of Motor Manufacturers and Traders (SMMT), the number of BEV models on sale has climbed to over 130 — up from 102 just one year ago.

This marks a record level of choice for British consumers and signals a clear shift in manufacturer priorities.

However, growing availability has not yet translated into proportionate demand. Battery electric vehicles accounted for just 20.4% of new car sales so far in 2025, falling short of the government’s Zero Emission Vehicle (ZEV) mandate, which requires each automaker to ensure that 28% of their new car sales are zero emission this year.

The result is a widening gap between what’s on offer and what’s being bought.

Electrification in the UK is no longer confined to premium brands or niche categories. The landscape now reflects a mass-market transition, with electric drivetrains available across the full spectrum of vehicle types and consumer price points.

Battery electric vehicles are now offered across every major segment of the UK car market — from compact city hatchbacks to executive SUVs and commercial vans. The spread of models covers a wider range of price points than ever before, reflecting both technological maturity and manufacturer scale-up.

The average BEV sold in the UK now delivers close to 300 miles of range on a single charge. Some models exceed 480 miles, more than double what the average UK driver covers in a week. Range is no longer a limiting factor in most use cases; it is now a competitive metric across multiple price tiers.

Electrification also extends well beyond battery-only vehicles.

Four out of five new car models available today feature some form of electrified powertrain — whether fully electric, plug-in hybrid (PHEV), or hybrid (HEV).

While BEVs are growing fastest, plug-in hybrids and hybrids still serve as transitional technologies, especially for buyers not yet ready to rely entirely on public charging. Their presence reinforces the broad shift underway: internal combustion is no longer the default.

The record number of battery-electric models on the UK market is not accidental. It’s the result of converging forces — regulatory clarity, accelerated tech development, and capital deployment across fleets and manufacturing.

Together, they have shifted the industry from compliance engineering to product diversification.

The UK’s commitment to net-zero emissions by 2050 and its plan to end sales of new petrol and diesel vehicles by 2035 have created clear boundaries for automakers.

These long-term targets, combined with the Zero Emission Vehicle (ZEV) mandate — which requires an escalating share of zero-emission sales from manufacturers each year — have reshaped product roadmaps. Portfolio planning has moved away from fossil-fuel longevity toward electrified volume and platform flexibility.

Rapid advancements in battery technology have made electric vehicles more competitive. Energy density has increased, charging speeds have improved, and thermal management is more efficient. These gains support the rollout of more models with longer range and faster turnaround times at the plug.

Simultaneously, infrastructure has scaled.

The UK now has over 55,000 public charging connectors, including more than 8,000 rapid chargers. The presence of more reliable infrastructure gives automakers greater confidence to bring diverse BEV products to market and support customers through the ownership cycle.

Fleets continue to lead the BEV adoption curve. Their demand for cost efficiency, regulatory compliance, and service uptime has pushed manufacturers to expand product lines to meet commercial needs.

This has had a spillover effect, accelerating product readiness and validation for broader markets.

More than £20 billion has been invested into zero-emission vehicle production across the UK, including retooled factories and new battery supply chains. These investments are anchoring domestic capability and creating a used EV pipeline that will eventually serve private buyers priced out of new models.

Model availability has scaled. Sales have not. While battery electric vehicles now account for 40% of new car model offerings in the UK, they represent just 20.4% of new car registrations.

This falls short of the government’s 2025 Zero Emission Vehicle (ZEV) sales mandate, which requires 28% of each manufacturer’s new car sales to be zero-emission. The bottleneck has shifted from supply to demand.

Manufacturers have done the work of expanding portfolios. BEVs are now present in every vehicle segment, with improved range, pricing diversity, and clear regulatory backing.

But consumers have not yet matched this acceleration. The sales gap suggests that retail adoption is the primary drag on market conversion.

Multiple friction points continue to slow the transition for private buyers. Upfront cost remains high compared to internal combustion equivalents, even with lower running costs. Charging infrastructure is growing but remains inconsistent in reliability, pricing, and geographic availability.

Taxation adds another layer of imbalance. Home charging is taxed at 5% VAT, while public charging carries the standard 20% rate. This discrepancy penalizes those without private driveways and risks deepening inequalities in EV access.

The Society of Motor Manufacturers and Traders (SMMT) continues to call for VAT reform and targeted purchase incentives to close the adoption gap.

While model diversity has reached record levels, the automotive industry argues that availability alone won’t drive mass adoption. The Society of Motor Manufacturers and Traders (SMMT) is calling for stronger fiscal measures to support the transition.

There’s never been a better time to go electric – with more choice, better vehicle range and improving infrastructure offering a compelling driving proposition. But the market still isn’t moving fast enough, so bold support for consumer EV uptake – notably investment in incentives and infrastructure – is needed to accelerate decarbonisation efforts and make switching open to all drivers.

Mike Hawes, SMMT Chief Executive

Manufacturers view the current product mix as progress, not endpoint. They argue that structural issues (cost, taxation, and public charging access) must be addressed to convert the model expansion into actual sales.

Without broader policy alignment, the supply-demand mismatch risks undermining the transition’s momentum.

The UK is positioned as one of the most electrified vehicle markets in the world by product offering.

More than 130 fully electric models are on sale, covering every major segment. With fleet demand rising and infrastructure improving, DriveElectric forecasts over 440,000 new BEV registrations by the end of 2025.

But the next phase of the transition won’t be defined by model count. It will be measured by how quickly retail buyers make the switch and how effectively policy removes remaining friction. The vehicles are here. The shift depends on who can access them, and how soon.